The Called Shot

Why I Believe December 2026 Gold Options May Be the Most Asymmetric Trade of the Decade

“You don’t get rich by diversifying into 50 mediocre assets. You get rich by finding 2 or 3 asymmetric home runs.”

— Stanley Druckenmiller

Oh, I remember it like it was yesterday.

That skinny yellow bat with the grip etched into it. The sound of the plastic ball whiffing and whizzing through the air as smoke from the grill drifted across the yard. Every Fourth of July, we built our own wiffleball Field of Dreams in the backyard. Baby pools served as the bases. A Slip ‘N Slide stretched into home plate. A cooler full of ice-cold beer stood behind the batter’s box as our makeshift strike zone. Neighborhood rivalries resurfaced, as everyone was jawing and talking trash.

For a few hours every summer, we were all the great bambino Babe Ruth. No steroids, just beer, adrenaline, and hotdogs. Pointing to center field, calling our shot and swinging for the fences.

And for those unfamiliar… no baseball story captures the imagination quite like The Called Shot.

During Game 3 of the 1932 World Series, after being heckled by the Cubs players, Babe Ruth allegedly pointed toward the center of Wrigley field before launching a towering home run exactly where he indicated. Nearly a century later, historians still debate what happened. Did Ruth actually call his shot? Was he pointing at the Cubs’ dugout? Was it all exaggerated after the fact?

The truth may never be known.

But what matters is what the story represents.

Conviction.

The willingness to stand in the batter’s box with two strikes… dig deep and swing for the fences while everyone else thinks you’re crazy.

Today, I believe investors may be staring at a modern version of The Called Shot.

Not in baseball.

In Gold.

Something Suspicious Is Happening

The accumulating evidence has led me to believe Gold is going to get revalued… and sooner than most think.

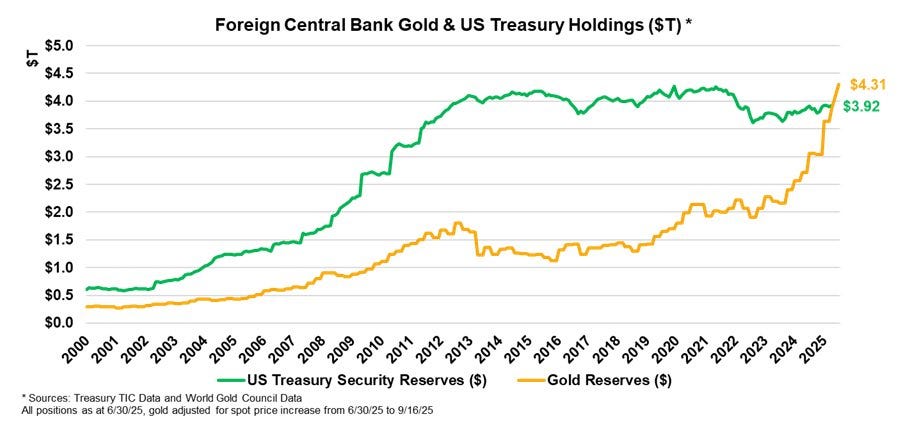

Bond yields are blowing out now. Central banks are buying gold at record levels. President Trump recently announced he wants to audit Fort Knox. States across America are reintroducing gold and silver into the monetary system.

And every single day, I watch one expiration:

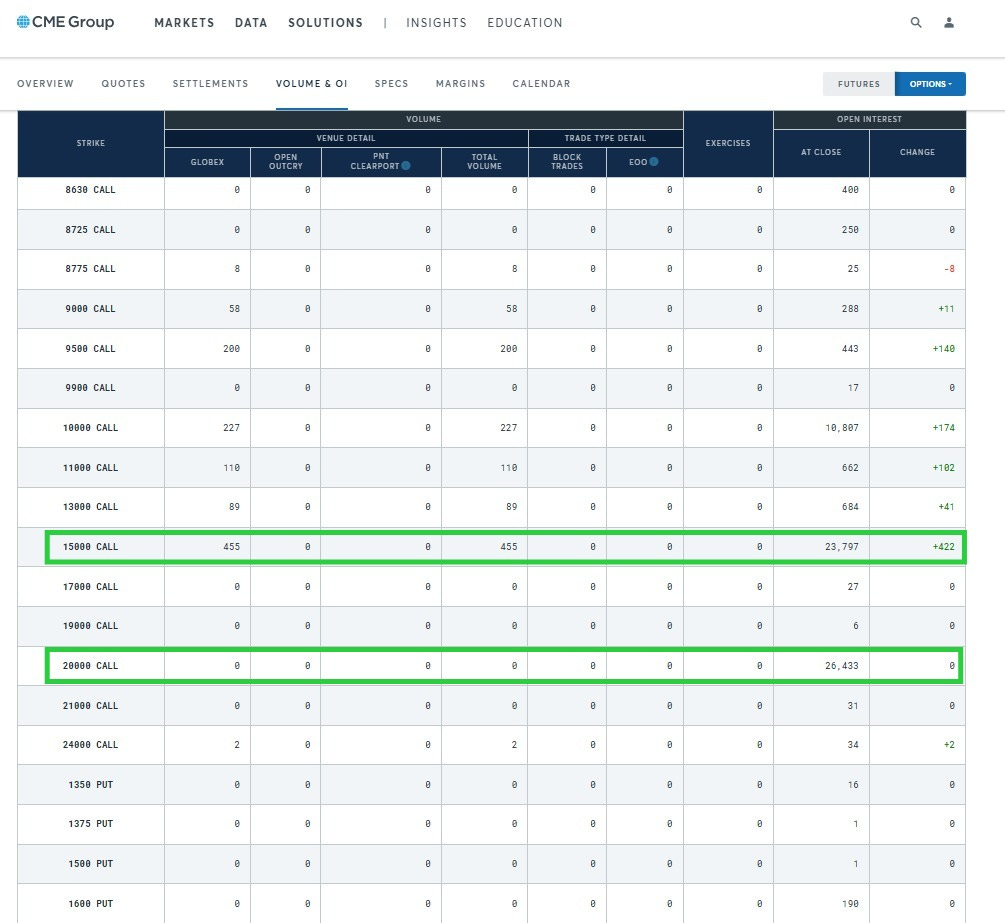

December 2026. Deep out-of-the-money COMEX gold calls.

$10,000/oz — 1.1M oz in open contracts

$15,000/oz — 2.4M oz in open contracts

$20,000/oz — 2.65M oz in open contracts

Thousands upon thousands of contracts.

The insiders tried to hide. But we found them.

The Fed Connection You Haven’t Heard About

Here’s where it gets even more interesting.

Kevin Warsh — the newly appointed Federal Reserve Chair — has quietly brought on a key adviser who authored the Project 2025 chapter on the Federal Reserve. That adviser is Paul Winfree.

And what does that chapter actually say?

I went directly to the source — the 900-page “Mandate for Leadership: The Conservative Promise 2025” published by The Heritage Foundation. Chapter 24, written by Winfree, lays out the case for radical monetary reform.

Here is what the document says:

“The process of commodity backing is very straightforward: Treasury could set the price of a dollar at today’s market price of $2,000 per ounce of gold. This means that each Federal Reserve note could be redeemed at the Federal Reserve and exchanged for 1/2000 ounce of gold—about $80, for example, for a gold coin the weight of a dime.”

That was written in 2023, when gold was $2,000/oz. Fast forward to today.

The government holds 261.5 million ounces of gold. If they revalue it from $42/oz to $15,000–$20,000/oz, they add $4–5 trillion to the balance sheet. That's enough to back a new gold-linked bond system without needing to buy more gold.

U.S. debt is $39 trillion. At $15,000/oz, U.S. gold reserves are worth roughly $4 trillion — about 10% of the debt. At $20,000/oz, that jumps to $5.2 trillion, or 13%. Not enough to fully back the debt, but more than enough to restore confidence and collateralize a new gold-linked bond system.

“One concern raised against commodity backing is that there is not enough gold in the federal government for all the dollars in existence. This is solved by making sure that the initial peg on gold is correct.”

In other words — revalue gold higher, and the math works.

“Beyond full backing, alternate paths to gold backing might involve gold-convertible Treasury instruments or allowing a parallel gold standard to operate temporarily alongside the current fiat dollar. These could ease adoption while minimizing disruption, but they should be temporary so that we can quickly enjoy the benefits of gold’s ability to police government spending. In addition, Congress could simply allow individuals to use commodity-backed money without fully replacing the current system.”

Winfree now serves as a temporary contractor for Warsh, assisting with policy analysis and special projects.

The chapter goes further, arguing that “the only permanent remedy is to take the monetary steering wheel out of the Federal Reserve’s hands and return it to the people.”

It presents three reform options, ranked in order of effectiveness:

Free banking — the Federal Reserve is “effectively abolished,” with banks issuing liabilities backed by gold or other commodities

Commodity-backed money — the dollar backed by “some hard asset like gold,” with the Fed maintaining regulatory functions

Rules-based policy — less radical reforms like the “K-Percent Rule”

Now, to be fair, Winfree has since tried to distance himself from the most extreme ideas in his own chapter. In a 2024 interview, he said: “I would not subscribe to the idea of nuking the Fed.”

And Warsh himself has pledged to uphold the Fed’s dual mandate… which sits in tension with some of Winfree’s published proposals.

Still.

The man who wrote the playbook for abolishing the Fed and returning to a gold-backed dollar is now advising the Fed Chair.

I’m sure it’s nothing.

“Golden” Dome for the White House

Now back to those COMEX Gold call options. Maybe they’re hedges. Maybe they’re volatility trades. Maybe they’re nothing at all.

But when you zoom out, the pieces begin fitting together in a way that’s difficult to ignore:

A Fort Knox audit

Judy Shelton’s gold-linked bonds

Sound money state legislation

Record central bank accumulation

A Fed Chair whose top adviser authored Project 2025’s “abolish the Fed, return to gold” chapter

And an options market quietly positioning for outcomes most investors consider impossible

Maybe these events are unrelated.

However, I believe we’re watching the early stages of the largest monetary transition of our lifetimes.

The old system is built on debt. The next system will require collateral to restore trust. And there is only one monetary asset sitting on sovereign balance sheets capable of filling that role.

Gold.

The CME Data Clue

Every day, I find myself checking the same expiration:

December 2026.

And every day, the open interest sitting on these deep out-of-the-money COMEX gold calls seems impossible to ignore.

The $15,000 calls.

The $20,000 calls.

Thousands upon thousands of contracts.

Notice the extraordinary concentration at the $15,000 and $20,000 call strikes, with open interest exceeding 23,000 and 26,000 contracts respectively. These positions dwarf neighboring strikes and strongly suggest institutional spread positioning.

What makes this unusual?

If traders were simply speculating on higher gold prices, open interest would likely be distributed across many strikes. Instead, open interest is overwhelmingly concentrated at the $15,000 and $20,000 strikes while intermediate strikes remain nearly empty.

This pattern strongly resembles a large institutional spread structure.

Most investors look at those strikes and laugh. After all, who in their right mind would bet on $20,000 gold?

But that’s the wrong question.

The right question is: Who is buying them?

Because somebody is. And not in small size.

The paired open interest strongly suggests institutional positioning. These aren’t random retail “lottery tickets”. The capital involved is sophisticated. For months these positions have continued to build.

The insiders tried to hide. But we found them.

In America, there are always insiders. The challenge is figuring out what they know.

Now, could these simply be hedges? Of course. Any serious analyst must acknowledge that possibility.

But when you combine:

Massive call positioning

State-level sound money legislation

Record central bank gold purchases

Fort Knox audit discussions

Sovereign debt stress

The possibility of gold-linked Treasury issuance

…you begin to see why some investors believe these positions may be signaling something larger.

Maybe they’re not betting on gold reaching exactly $20,000. Maybe they’re betting on a monetary event that would make such prices conceivable. Maybe they’re positioning for a volatility explosion. Maybe they’re preparing for a revaluation.

I cannot prove that’s what these trades represent. Neither can anyone else.

But I do know this:

The market rarely spends millions of dollars preparing for events it believes are impossible.

And every day that December 2026 open interest continues to grow, the question becomes harder to ignore.

The Missing Piece

The obvious question is: Why would anyone care about a gold revaluation in the first place?

Because the real problem isn’t debt. It’s the optics of confidence.

For decades, long-term Treasury bonds have been treated as risk-free assets. But what happens when investors begin questioning that assumption? What happens when inflation, deficits, and duration risk make long-term sovereign debt increasingly difficult to sell?

The Treasury needs buyers. More importantly, it needs confidence.

That’s where the parallel system of gold-linked bonds enters the story.

Gold bonds are not about replacing Treasuries. They are about making Treasuries sellable again. A gold-linked bond gives investors exposure to U.S. sovereign credit while attaching a hard-asset anchor to the promise. In effect, gold becomes collateral for confidence.

Viewed through that lens, a gold revaluation starts making a lot more sense. Not because policymakers suddenly want a gold standard. But because confidence may become the most valuable asset on the government’s balance sheet.

Here’s how it could actually happen:

The Treasury loses buyers for conventional long-term debt.

To restore demand, it announces gold-linked bonds. But to make those bonds credible, the U.S. must revalue its official gold holdings from the current $42/oz to near market prices.

That revaluation creates a wave of price discovery across COMEX futures, forcing settlement at levels far higher than anyone expects—potentially $15,000–$20,000/oz.

If that sounds extreme, good. That’s why the options are cheap.

And if that’s the case, the unusual December 2026 positioning becomes far more interesting.

Maybe these traders are hedging. Or maybe they’re positioning for a world where gold once again plays a monetary role.

That’s the question I keep coming back to. And it’s also why I’m putting real money behind this thesis.

PREMIUM CONTENT BEGINS HERE

To read the specific trade mechanics, position sizing, exact options structure, and risk management checklist, upgrade to a paid subscription.