Export Controls Tighten, Physical Metals Break Out, and Supply Takes Control – Macro Market Report

Key Charts: Stocks, Oil, Gold, Silver, Miners, DXY, and Bitcoin — What to Watch This Week

📣 If this report helped you see how markets are shifting from price discovery to supply control, share it with someone who still thinks this is a “normal cycle.”

🌎 Big Picture

This week marks a clear shift from price discovery to supply control.

Export licenses, industrial subsidies, exchange risk controls, and even disputes over gold ownership all point in the same direction: governments are no longer relying on open markets to secure critical materials.

China is locking down metals and subsidizing domestic production. Western capital is front-running scarcity through ETFs. Trade flows are shrinking, not normalizing. Gold is quietly re-entering politics.

This is not about rate cuts or inflation cycles.

It is about who controls supply, who absorbs volatility, and who bears risk as global markets fragment.

Price still matters…but access now matters more.

🌍⛔ 1. 2026 Export Controls on Strategic Metals Signal a New Phase of Resource Nationalism

Governments are moving decisively toward formal export controls on strategic metals beginning in 2026, accelerating a global shift away from free-flowing commodity markets and toward state-managed supply.

Licensing regimes, quotas, and domestic prioritization are replacing open exports. Silver, copper, rare earths, and specialty industrial metals are increasingly treated as national security inputs, not trade goods.

What makes the 2026 timeline critical is coordination. Importing nations are blocking access through tariffs and regulation, while exporting nations are responding by locking supply at the source.

Once export licensing frameworks are in place, metals markets stop clearing globally.

They begin clearing politically.

This marks the end of globalization as a pricing mechanism for strategic materials.

🇨🇳🪙 2. China Moves to Restrict Silver Exports Beginning January 2026

China is preparing to implement a silver export licensing framework starting January 2026, breaking decades of relatively unrestricted silver exports to global markets.

An estimated 50–70% of global silver supply has historically flowed through Chinese mining, refining, and export channels. Licensing allows Beijing to control how much silver leaves the country and when… prioritizing domestic availability over global liquidity.

This mirrors China’s approach to gold, rare earths, and energy inputs:

• Strategic stockpiling

• Reduced exposure to Western exchanges

• Domestic control of physical settlement

Silver is not being treated as a commodity.

It is being treated as strategic infrastructure.

For Western markets, this raises structural vulnerability to demand shocks and regional supply shortages.

🇨🇳💻 3. China Prepares Up to $70 Billion in Semiconductor Incentives as Tech Decoupling Accelerates

China is considering a sweeping incentive package of up to $70 billion to support its domestic semiconductor industry, including 200–500 billion yuan in subsidies and financing support.

This is not stimulus. It is industrial mobilization.

Semiconductors now sit alongside energy and metals as core national-security assets. By backing firms such as Huawei and Cambricon, China is accelerating a parallel technology ecosystem designed to operate independently of Western inputs.

The metals implication is critical:

• Chip manufacturing is metals-intensive

• Silver and copper demand becomes locked-in

• State funding insulates demand from price cycles

China is not chasing efficiency.

It is securing physical capability and control.

📈🪙 4. ETF Inflows Surge Across Precious Metals as Institutional Demand Accelerates

Exchange-traded funds added 351,765 troy ounces of gold in a single session, the largest one-day inflow since October, bringing year-to-date net purchases to 14.8 million ounces, according to Bloomberg.

This is not retail speculation. It is institutional allocation.

Notably, inflows are accelerating:

• Ahead of expected rate cuts

• Near price highs

• Across silver, platinum, and palladium

ETF demand is now confirming physical stress rather than lagging it. Capital is rotating toward assets that sit outside the credit system as balance-sheet risk rises and geopolitical fragmentation deepens.

Gold remains the monetary anchor.

The rest of the complex is being pulled into the same orbit.

🇨🇳🥈 5. Chinese Silver Fund Warns of Risk as Domestic Premiums Blow Out

The UBS SDIC Silver Futures Fund (LOF) has issued formal risk warnings as it trades at a ~12% premium to its underlying assets… a record divergence versus Shanghai Futures Exchange contracts.

On the surface, this looks speculative. In reality, premium blowouts emerge when:

• Physical availability tightens

• Access to metal becomes constrained

• Capital is forced into proxy vehicles

This is regional repricing, not global excess.

Western silver stress showed up in London vaults.

Chinese stress is now appearing inside domestic investment vehicles.

Speculation can cool.

Physical scarcity does not.

🇨🇳🥈 6. Shanghai Futures Exchange Tightens Silver Trading Limits as Volatility Accelerates

The Shanghai Futures Exchange announced new risk-control measures effective December 12, 2025, raising both margin requirements and daily price limits for silver futures.

Key changes:

• Daily price limit expanded to 15%

• Hedging margin raised to 16%

• Speculative margin raised to 17%

These measures are deployed when exchanges expect instability, not calm.

Higher margins restrict leverage. Wider limits allow price discovery. Together, they signal preparation for larger, more volatile moves.

This is volatility management, not suppression.

When exchanges intervene this way, it usually means the underlying market is no longer behaving normally.

🇺🇸📉 7. U.S. Trade Deficit Shrinks to Smallest Level Since 2020… For the Wrong Reasons

The U.S. trade deficit narrowed nearly 11% month over month to $52.8 billion, the smallest since mid-2020.

This is not resurgence.

It is inward contraction.

Import demand is softening under higher prices and policy barriers. China is rerouting exports elsewhere. The U.S. is structurally insulating itself from imported deflation.

Historically, shrinking trade deficits under these conditions align with:

• Slower real growth

• Persistent domestic inflation

• Greater reliance on fiscal and monetary support

The deficit is shrinking… inside a system that still requires continuous monetization.

🇮🇹🟡 8. Italy’s Gold Reserves Become a Political Fault Line Inside the Euro System

Italy’s finance minister has discussed a proposal to legally declare the country’s 2,452 tonnes of gold as the property of the Italian people, not solely the central bank.

The ECB has pushed back, warning of political interference and ambiguity.

This is not about selling gold.

It is about control and legitimacy.

Gold inside the euro system has long existed in a legal gray zone. By reframing ownership, Italy is challenging centralized monetary authority at a time of rising fiscal strain.

Gold is no longer a relic.

It is re-entering politics as sovereign collateral.

🔑 Key Market Themes & Weekly Asset Movements

S&P 500 & Nasdaq – U.S. equities ended the week modestly lower. The S&P 500 closed Friday at 6,827, drifting into resistance on notably light volume. The Nasdaq Composite also finished slightly weaker, closing at 25,196, with upside momentum fading near recent highs.

Gold – Gold regained upside traction, advancing to $4,257 and pressing against breakout levels. The move continues to be driven by sustained central-bank accumulation, rising expectations for rate cuts, and renewed safe-haven demand as market volatility increases.

Silver – Silver closed Friday near all-time highs at $61.92. Ongoing physical tightness, persistent backwardation, accelerating official-sector accumulation, and rising industrial demand continue to reinforce an increasingly bullish, supply-constrained structure.

GDX (VanEck Gold Miners ETF) – Gold miners remain well supported by elevated bullion prices and improving investor interest. Following a healthy pullback, the sector has regained momentum and broken back above resistance, with GDX closing Friday retesting the $85.66 level.

SLVP (iShares MSCI Global Silver & Metals Miners ETF) – Silver miners are breaking out above major resistance, supported by tightening supply-demand dynamics across the silver complex. Price action closed Friday retesting resistance at $33.19, though the session finished on a bearish candle.

Crude Oil – Crude oil futures weakened further, settling at $57.52 per barrel on Friday. Prices remain under pressure amid oversupply concerns and signs of softening global demand.

U.S. Dollar (DXY) – The dollar eased on Friday, with DXY pulling back to 97.97 as softer macro data weighed on the currency. 2026 Rate-cut expectations continue to cap upside, leaving the broader outlook mixed and directionally uncertain.

Bitcoin – Bitcoin ended the week modestly lower, closing Friday at $90,275. Despite a strong advance earlier in the year, the digital-asset complex remains volatile, with uneven momentum and fragile sentiment.

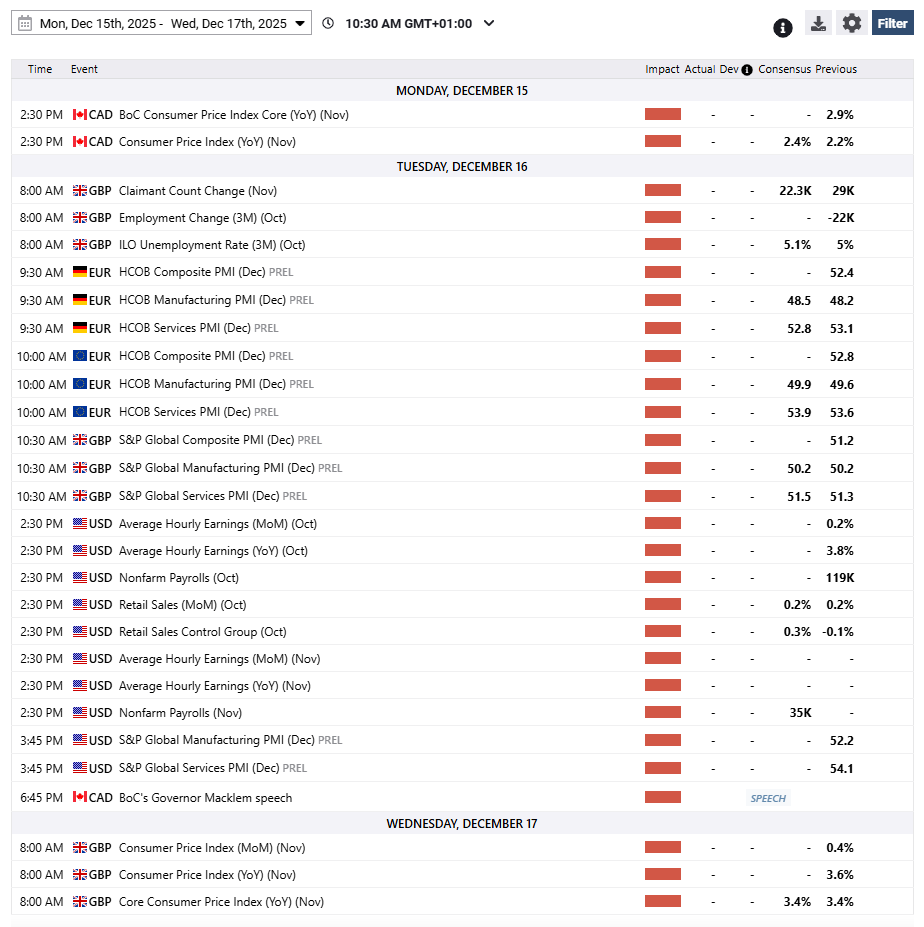

🗓️ Economic Calendar — Key Events This Week

CAD – Monday, December 15

BoC Core CPI (YoY, Nov)

Canada CPI (YoY, Nov)

GBP – Tuesday, December 16

Claimant Count Change (Nov)

Employment Change (3M, Oct)

ILO Unemployment Rate (3M, Oct)

S&P Global Composite PMI (Dec, Prelim)

S&P Global Manufacturing PMI (Dec, Prelim)

S&P Global Services PMI (Dec, Prelim)EUR – Tuesday, December 16

HCOB Composite PMI (Dec, Prelim)

HCOB Manufacturing PMI (Dec, Prelim)

HCOB Services PMI (Dec, Prelim)USD – Tuesday, December 16

Average Hourly Earnings (MoM, Oct)

Average Hourly Earnings (YoY, Oct)

Retail Sales (MoM, Oct)

Retail Sales Control Group (Oct)

Nonfarm Payrolls (Nov)

S&P Global Manufacturing PMI (Dec, Prelim)

S&P Global Services PMI (Dec, Prelim)CAD – Tuesday, December 16

BoC Governor Macklem SpeechGBP – Wednesday, December 17

Consumer Price Index (MoM, Nov)

Consumer Price Index (YoY, Nov)

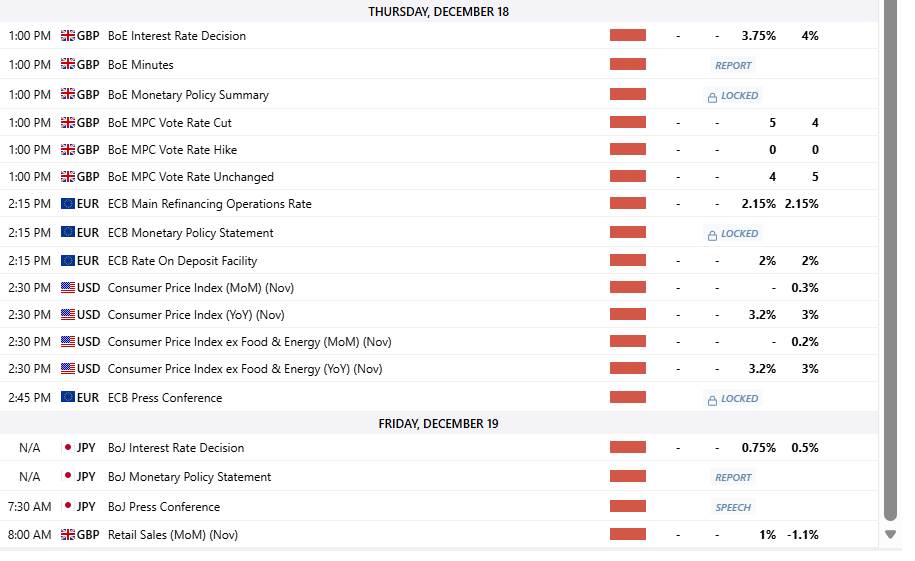

Core CPI (YoY, Nov)GBP – Thursday, December 18

BoE Interest Rate Decision

BoE Monetary Policy Summary

BoE Minutes

BoE MPC Vote (Rate Decision)EUR – Thursday, December 18

ECB Main Refinancing Operations Rate

ECB Deposit Facility Rate

ECB Monetary Policy Statement

ECB Press ConferenceUSD – Thursday, December 18

Consumer Price Index (MoM, Nov)

Consumer Price Index (YoY, Nov)

Core CPI ex Food & Energy (MoM, Nov)

Core CPI ex Food & Energy (YoY, Nov)JPY – Friday, December 19

BoJ Interest Rate Decision

BoJ Monetary Policy Statement

BoJ Press ConferenceGBP – Friday, December 19

Retail Sales (MoM, Nov)

📊 Featured Chart Breakdown

Silver/USD (Daily Chart)

Trend: Bullish

Support: $59.33

Resistance: $64.65

Entry Zone: Buy under $57.36 and anything lower. Target $52.85

Watch: Henka-Bi Time Cycle December 15th

Silver has now broken out above resistance, confirming the bullish setup from last week. Price pushed cleanly above the $59.33 level and is now trading higher, keeping the broader uptrend intact.

Silver is currently trading in the $63–64 area, which is an important short-term decision zone. Momentum remains strong, but price is stretched in the near term. This increases the chance of either:

• A short pause or pullback to let the market cool off, or

• A continued push higher if buying pressure stays strong

Both outcomes are normal after a breakout.

The next Henka-Bi timing window arrives around December 29, which marks the next key point where silver is likely to either resume its advance or complete a healthy reset before the next leg higher.

Key Levels to Watch

Former Resistance (Now Support):

• $59.33

Upside Targets:

• Near-term target: $63.37 (already reached / in progress)

• Next major target: $68.49

Pullback Support Levels:

• First support: $57.36

• Stronger support: $55.11

• Deeper support: $52.59

As long as silver stays above $57–55, the bullish trend remains healthy. Any pullback into this area would be considered normal and constructive, not a breakdown.

The big picture remains clear:

The trend is up.

The breakout is confirmed.

Volatility is increasing.

Silver has moved from waiting to move into actively trending, with higher prices likely after the market digests recent gains.

This is no longer a question of whether silver is bullish…

it is about how the market resets before the next move higher, with December 29 as the next important timing checkpoint.

The historic quarterly close has laid the foundation… the next leg is imminent.

📈 For full context, see my Silver Bull Market Roadmap, which outlines the macro thesis, key Ichimoku levels, and trading framework behind this move.

💡 New to Ichimoku?

Grab my audio & eBook “At One Glance: Master the Ichimoku…” — it breaks down my charting method with real examples and setup logic.

Hurry! First 100 People use Discount code: GREYEDGE25

🔒 Premium Analysis

👇 What’s behind the paywall:

✅ Full Ichimoku chartbook: BTC, SP500, Gold, Silver, Oil, GDX, SLVP, DXY

✅ Key support/resistance zones + Henka-Bi Time Cycle Windows

✅ Actionable trade plans and targets

✅ Weekly macro catalyst watch